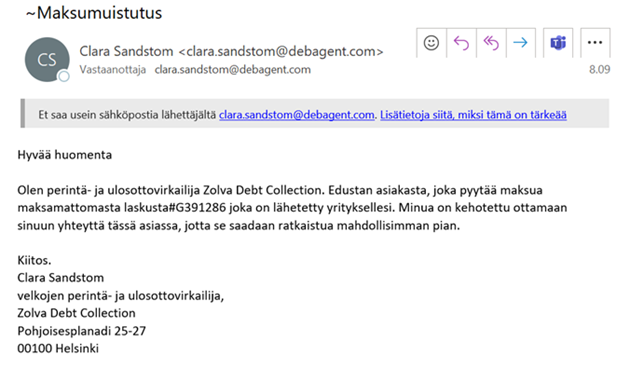

We have received information that various scam messages are circulating in the name of Zolva. You may find more information about scam messages by clicking on this link.

Scam messages have been sent at least by e-mail and demand to pay the debt.

We have received information that various scam messages are circulating in the name of Zolva. Scam messages may look genuine and may contain the Zolva logo. Scam messages have been sent at least by e-mail and demand to pay the debt.

The fraudulent messages have been reported to the police.

If you have received an email that you suspect is a scam, delete it without opening any attachments.

Do not reply to the message.

Do not open links or attachments in the message.

You don’t need to do anything else about it.

If you doubt the authenticity of the message you received, you can check the matter by contacting our customer service at asiakaspalvelu(at)zolva.com.

This message has not been sent by Zolva:

The scam messages were originally reported on 14.11.2023 and the news has been published again today on 21.11.2023 after Zolva received information about the new scam messages.

Zolva is the first to launch in Finland: Debt collection performance data is now transparent and up-to-date for creditors

25 Aug 2023, 8:03 GMT

Zolva's goal is to make the debt collection industry more transparent. Producing analyzed information for customers is an important step towards a transparent debt collection industry.

Zolva has established a cooperation with the Swedish analysis company Dignisia. The analyzed information helps companies to make more accurate forecasts, ensures predictability and optimized cash flow from non-performing loans.

Debt collection company Zolva sets up high standards in the transparency of debt collection services when the company begins cooperation with the Swedish analysis company Dignisia.

“The change to the industry’s practices is big, because companies usually only see the customer base that is in debt and how much has been paid.”

LAURI KOSLOFF, HEAD OF FINANCE

According to Zolva’s Head of Finance Lauri Kosloff, the cooperation enables visibility to payment behaviour of non-performing receivables on customer specific level and enables analyzes for each customer group. It is important for creditors to understand the quality and performance of their non-performing portfolios. In optimal cooperation with the debt collection agency, the activities are agreed and optimized together and the best time to sell the non-performing receivables is optimized based on performance of the portfolio(s).

In addition, the sales of non-performing portfolios to debt collection agencies are made easier when the credit institution or the invoicing entity has good data, which increases trust between the seller and the buyer and enables good dialogue between the parties.

Dignisia analyzes and refines information almost in real time. It is a value-added service for companies using Zolva’s services.

– The change to the industry’s practices is big, because companies usually only see the customer base that is in debt and how much has been paid. In the future, companies utilizing Zolva’s services will also know how efficiently Zolva’s different collection stages work. Collection should be optimized by considering the cashflow from non-performing receivables and generated costs for collection activities, says Kosloff.

According to him, the Dignisia’s service will especially benefit financial companies and the telecom sector, which have large invoicing volumes and for which cash flow and credit losses play a significant part in their result.

– The data provided by Dignisia enables companies utilizing Zolva’s services to benchmark the effectiveness of the measures and activities of two different debt collection agencies. Then everything is transparent, says the Head of Finance.

Transparency is common goal of Dignisia and Zolva

Dignisia, which operates internationally, has a good understanding of the needs of debt collection industry, as the company’s management has previously worked in various management positions at different debt collection agencies.

One of Dignisia’s most important goals is to bring more transparency to the collection industry through technology. Transparency develops cooperation between debt collection agencies and creditors, brings results and improves the customer experience. In addition, technology gives company management the opportunity to make data driven decisions based on analyzed information.

– The debt collection industry has lacked flexibility, transparency, and customer centricity for a long time. Especially now, when the interests of sellers and buyers in the non-performing portfolio -market have not met at a sufficient level. In our opinion, Dignisia produces the best reporting in the industry and allows benchmarking between different debt collection agencies. We think Dignisia’s service supports Zolva’s vision and represents prefectly in which direction the debt collection industry should change, says Zolva’s Head of Sales Olli Jumeneff.

According to him, the cooperation between Zolva and Dignisia results value adding services, which will add significant value to the business of credit institutions or other creditors.

– When we combine Zolva’s know-how, modern technology and Dignisia’s best practice -reporting, we are able to offer the best offering on the market, especially for the credit institutions.

Zolva in brief

Founded in 2021

Previously known as Finans2 in Nordics

Group’s revenues in 2022 48 MEUR

650 employees

Operations in Norway, Finland, Sweden, Denmark, Italy, Spain and Portugal

Dignisia CEO Gustav Terland says that the cooperation between the two companies has started very well. According to the CEO, Dignisia’s customers are utilizing Dignisia’s data, for example, when optimizing receivables management and debt collection activities, managing risk, and developing responsible lending.

– We are an independent operator within debt collection industry and in discussions with the people of Zolva, we understood that they want to achieve the same goals as us. Zolva wanted to offer its customers something new and we can add value throughout Dignisia’s services.

Changes to interest rate cap and Consumer Protection Act

05 May 2023, 5:33 GMT

The planned changes to the Consumer Protection Act and the interest rate cap have been confirmed on March 23. The changes will take effect on October 1.

The changes approved to the interest rate cap and the Consumer Protection Act will have the most significant effects on payment service companies that offer consumers the option to pay by invoice or in installments.

Confirmed amendments to the Consumer Protection Act on March 23, 2023 contain various changes, e.g. to the interest rate ceiling, good lending practices, the order of payment methods offered in the online store and the obligation to identify purchases made with an invoice in the online store with strong authentication (SCA). The changes enter into force on 1 October 2023.

The changes will especially affect payment service companies that have offered consumers the opportunity to pay for their online purchases by invoice or in installments with an interest rate of more than 15%. In addition, the changes will have an impact on certain credit cards and unsecured consumer loans.

When the Consumer Protection Act changes on 1 October 2023, the new interest rate ceiling will be the reference interest rate according to the Interest Rate Act plus 15 percentage points.

However, in the law that enters into force, the total interest rate on the loan may not exceed 20 percent at any point.

What will change?

The order of payment methods presented in online stores

The obligation to verify the consumer’s identity with SCA when the consumer buys from an online store with an invoice

The interest rate cap on consumer loans will be reduced from the current 20 percent to 15 percent

Good lending practice, especially in relation to credit marketing and late payment situations

The order of available payment methods in online stores

In the future, online retailers and payment service companies must present the available payment methods to the consumer in the following order:

Payment methods that do not include the possibility of applying for or using credit or deferred payment

Payment methods, which may include the possibility to apply for or use credit or deferred payment

Payment methods that mean applying for credit, using it or have possibility for deferred payment

According to the government’s proposal (HE 218/2022), payment methods that do not include the possibility to apply for or use credit or receive other payment deferrals typically mean so-called online payments, where the consumer’s account is debited immediately in connection with the purchase, as well as e.g. payments made with debit cards or sports or cultural benefits. If, in connection with the online payment offered by banks, the consumer also has a credit account to choose from, this alone does not lead to the fact that the online payment cannot be considered a payment according to section 1.

The purpose of the law is that in the order in which the payment methods are presented, online bank payments must be presented first, card payments and mobile payments second, and lastly an invoice or various installment payment options.

Verification of the identity of the consumer online

The Consumer Protection Act has previously stipulated that when drawing up a credit agreement, the creditor must verify the consumer’s identity with strong identification.

Some of the operators offering payment services have defined purchases made with an invoice as being excluded from Consumer Protection Act chapter 7 and considered that deferred payment as such is not considered a credit according to Consumer Protection Act chapter 7. According to the view of these operators, the purchases made with the invoice have not formed a credit agreement and thus the creditor has not had the obligation to verify the identity of the consumer through SCA.

Payment service companies have justified their practices, e.g. with various other identification mechanisms, the usability of the services and conversion improvement.

After the change in the Consumer Protection Act on October 1, 2023, the consumer must be identified with SCA whenever the consumer buys online in a way that means deferred payment.

The extension to the identification obligation improves the consumer’s position, the safety of purchasing online, and clarifies the identification practices between different payment methods.

Banks’ strong identification practices, e.g. through applications have developed significantly in recent years. Nowadays, it is difficult to justify the lack of strong identification with usability and conversion improvement.

Changes to the interest rate cap

In the past, an interest ceiling has been applied to consumer loans, which has been limited to 20 percent, including the reference interest rate according to the Interest Rate Act. When the Consumer Protection Act changes on 1 October 2023, the new interest rate ceiling will be the reference interest rate according to the Interest Act plus 15 percentage points. However, in the law that enters into force, the total interest rate on the loan may not exceed 20 percent at any point.

In an article previously published by Zolva, the rapid turnaround in unsecured credit interest rates has been reviewed. For new withdrawals, the average interest rate has risen to 11 percent. Looking at the statistics on credit interest rates published by the Bank of Finland, one might assume that the change is not significant, but the change will probably limit the possibility of certain consumers to get credit.

The most significant effect of the interest rate change will be on online shopping payment service companies that offer payment options by invoice and in installments, and whose interest rates have generally been close to 20 percent. In addition, the interest rate cap will have effects on certain credit cards and unsecured consumer loans where the interest charged has been over 15%.

Rapid growth in interest rates on unsecured consumer loans

, 5:32 GMT

Olli Jumeneff predicts that interest rates on unsecured loans will continue to rise.

The interest rate on new unsecured loans has risen rapidly to more than 11 percent on average. Zolva’s Olli Jumeneff encourages consumers to be careful with their finances.

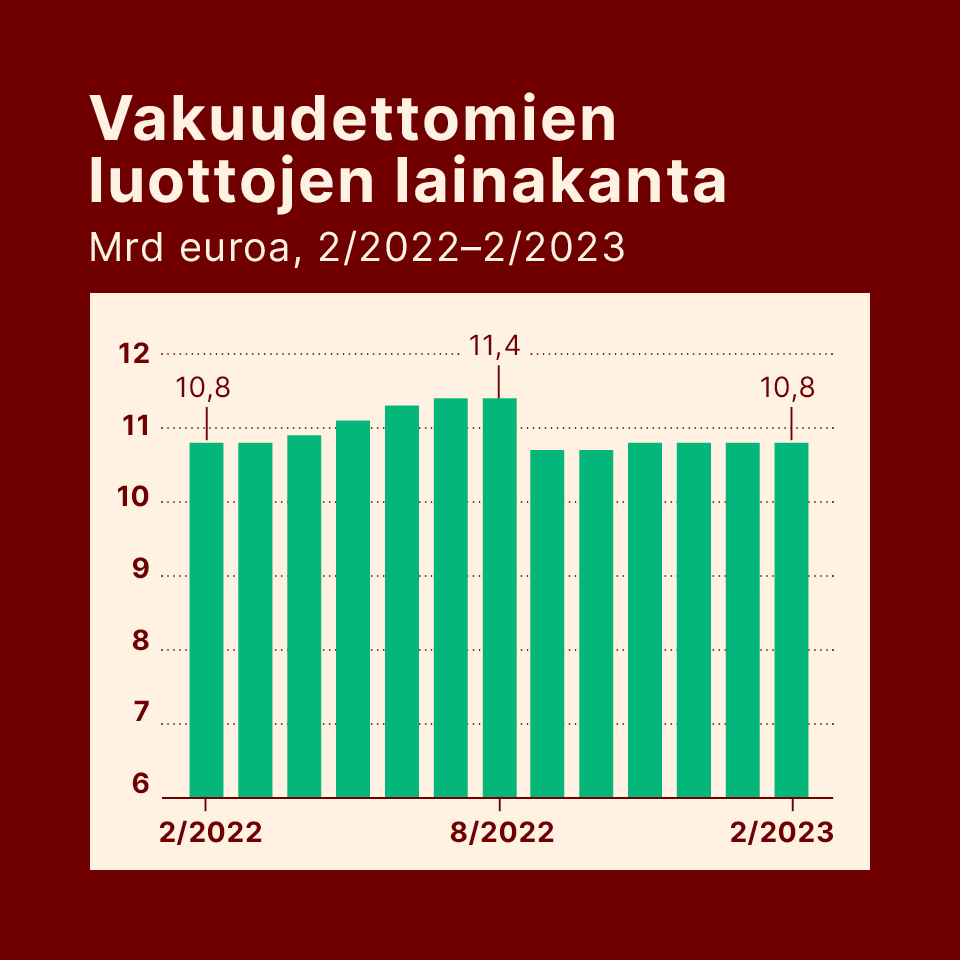

High inflation has reflected quickly in interest rates. The rise in interest rates can also be seen in unsecured consumer loans, in which loan portfolio in Finland is around 11 billion euros (February 2022, 11 billion euros). The unsecured loan portfolio of household consumer loans is about 8.5 billion (8.2), when loans related to the purchase of financing registered vehicles are removed from the figures.

According to Olli Jumeneff, Head of Sales of debt collection agency Zolva, the average interest rate on credit lines including credit cards and other unsecured consumer loans is currently around nine percent (6.6). Looking further down the line in the figures, the average interest rate on new consumer loans has already risen to 11 percent (8).

Jumeneff demands control from consumers in their consumption and personal economy. The danger is overindebtedness.

– Inflation drives up costs everywhere. The need for consumer loans increases if consumers do not have enough buffers in their personal economy.. The situation is also challenging for companies, as our latest CFO-Barometer shows. It is difficult for companies to pass on price increases in their entirety to customers, even though costs have risen significantly in a short time. It weakens profitability and affects employment rates, he says.

According to Asiakastieto, more than 365,000 (389,000) Finns have a payment defaults in their credit information, even though the amendment to the Credit Information Act that came into effect at the end of last year removed almost 20,000 people from the register.

Jumeneff predicts that the interest rate peak has not yet been seen.

– The European Central Bank’s increases in the reference interest rate do not alone explain the increase on unsecured consumer loan interest rates. Lenders also face cost pressures from elsewhere, and the rise in funding costs for lenders is greater than the rise in the reference interest rate. In that case, the costs cannot be transferred in their entirety to credit interests of consumer loans, he continues.

Legal changes to slow down overindebtedness

Unsecured consumer loans refer to loans for which no guarantee or other security has been given as collateral. Such loans are common, for example, in home renovations or home appliance purchases.

Jumeneff says that the most significant measure in the fight against overindebtedness is a positive credit information register. Its utilization in lending will begin on April 1, 2024.

A positive credit information register means that all lenders are obliged to report the credits taken by the consumer to a common register maintained by the authority. Credit register data can be combined with income register data.

In the future, lenders will know how much credit the consumer has to various financial institutions and what his ability to pay is in relation to the amount of credit.

Jumeneff says that this increases transparency and helps responsible lending. I hope this means that the payment of previous credits with new credit will decrease, and through this, customers will have a better chance to settle their debts at the latest through collection or foreclosure, when the over-indebtedness can be stopped as early as possible.

In addition, there is an amendment to the Consumer Protection Act that will lower the maximum interest rate on consumer loans from the current 20 percent to 15 percent. The law enters into force on 1 October 2023.

– The change in the maximum interest rate will exclude some consumers from the market. However, with the current reference interest rate of the European Central Bank, we do not see a significant difference in the total interest paid by the consumer. Previous interest rate regulations have led to the fact that the average capital of loans has increased, when a higher return is desired from one customer. I don’t see this development as a good thing. I would hope that official reporting and published statistics would also take into account the average capital of loans, so that decision-makers can better monitor the development of the consumer credit market and the effects of various measures, says Jumeneff.

Zolva in brief

Founded in 2021

Previously known as Finans2 in Nordics

Estimated revenues of the group are 50 MEUR

650 employees

Operations in Norway, Finland, Sweden, Denmark, Italy, Spain and Portugal

Inflation as a headache for CFO’s: One concern is emphasized

05 Apr 2023, 10:07 GMT

Lauri Kosloff says that high inflation has come as a shock to some companies.

Based on Zolva’s CFO-Barometer, transferring price increases driven by the inflation to customers is challenging in the current economic situation.

Debt collection agency Zolva’s CFO-Barometer asked what kind of challenges high inflation causes for your companies business? In the open answers, one thing was emphasized above all others: implementing price increases for different customer groups is somewhat challenging.

“Companies do not see price increases as an easy solution to cover increased production costs.”

LAURI KOSLOFF, CFO

Other concerns were, for example, the effect of the already raised prices on general consumption, fuel prices, the difficulty of forecasting, high pressure for wage increases, increased funding costs and the weakening of profitability.

According to Zolva’s CFO Lauri Kosloff, the inflation levels have come as a shock to some of the companies.

– Even though the media has talked about the increase in consumer prices, companies do not see price increases as an easy solution to cover increased production costs, as there is competition in the market. Consequently, the impact of high inflation on businesses is and will be one of the biggest challenges after the pandemic, says Kosloff.

According to Statistics Finland, the annual increase in consumer prices was 8.4 percent in January. Inflation is predicted to remain high for upcoming months.

Inflation is also one of the biggest explanatory factors why the Economic pulse of the CFO-Barometer remained at modest 62 points. The pulse of the Finnish economy describes the growth and profitability prospects of the largest companies in the next three months.

As many as 40 percent of the CFO’s who responded to the CFO-Barometer predicted that growth and profitability will remain weak or avoidable.

Zolva’s CFO-Barometer measures the Finnish economic pulse

– Through the survey and economic indicators, you can see how companies have already reacted to the changing environment. In this case too, the business field is divided into many different sectors and the measures vary according to the industry, company size and the company’s financial situation, says Kosloff.

He estimates that high inflation and the challenges of companies will inevitably affect the development of employment rates. On the other hand, there are always companies that swim upstream.

– The most opportunistic companies see cost pressures as an opportunity to increase their market share.

Zolva’s CFO-Barometer was implemented in February as an online survey. There were 33 respondents. The next barometer survey is in April and the results of the survey will be published in May.

Zolva in brief

Founded in 2021

Previosuly known as Finans2 in Nordics

Group’s estimated revenues are 50 MEUR

650 employees

Operations in Norway, Finland, Sweden, Denmark, Italy, Spain and Portugal

Pulse of Finnish economy is now 62 – This is what it tells

04 Apr 2023, 7:31 GMT

Zolva's CFO-Barometer describes CFO's views on the economic development of large companies.

Debt collection agency Zolva’s first CFO-Barometer has been published. The answers of the CFO’s of Finland’s largest companies are highly fragmented.

Faith of CFO’s at Finland’s largest companies in the growth and profitability of will be tested in the coming months. As many as 40 percent of the CFO’s who responded to the debt collection agency Zolva’s CFO-Barometer predicts that growth and profitability will remain weak or modest in next three months.

“High inflation and consumer caution will certainly have a debilitating effect on the results of the pulse.”

LAURI KOSLOFF, TALOUSJOHTAJA

Taking into account all the answers, the economic pulse of companies remained at 62 points. The deviation in the answers was wide, as the lowest score was 20 points and the highest was 96. The maximum score was one hundred.

Zolva’s CFO Lauri Kosloff considers the large deviation in the answers surprising and worrying.

– In some companies, the results are indicating strongly deteriorating situation and even difficulties in terms of continuing business operations. The barometer produced by the Confederation of Finnish Industries also supports the view of companies’ low expectations. High inflation and consumer prudence will certainly have a debilitating effect on the results of the pulse. Financial decision-makers are generally a bit cautious in their estimates, especially regarding growth, says Kosloff.

The scoring of Zolva’s CFO-Barometers’ has been done in such a way that 0–10 points means the risk of going bankrupt. On the other hand, 11–30 points is weak, 31–49 points is to be below average, 50–75 points is satisfactory, 76–85 is good and more than 85 points is an excellent level.

Dividing into two groups in investments

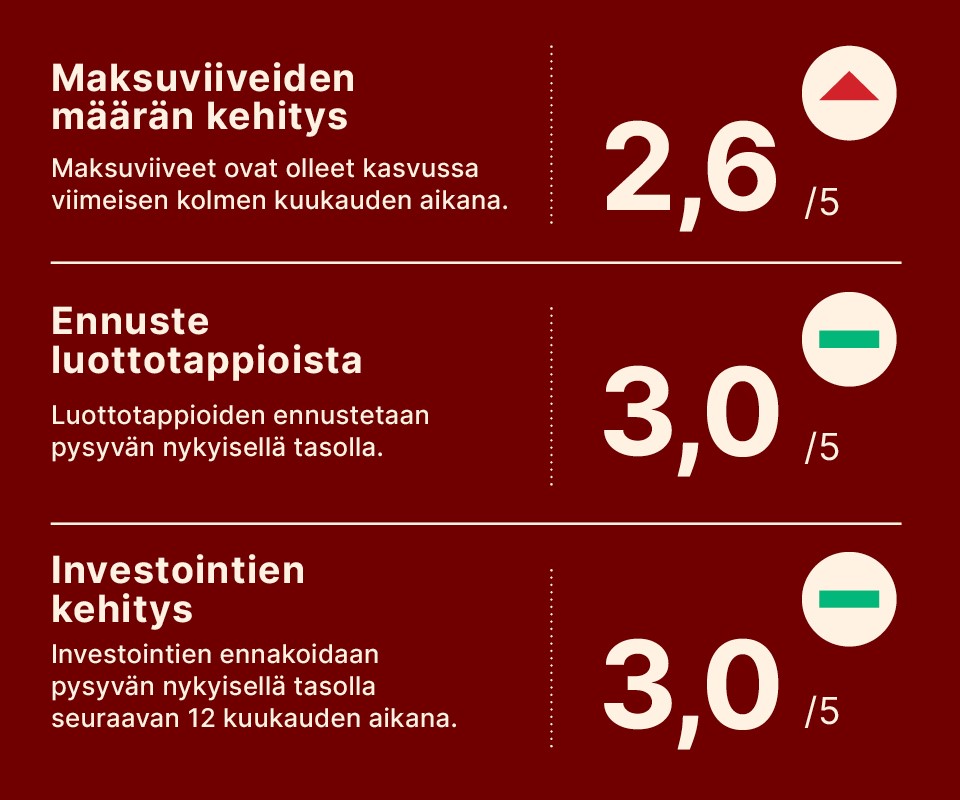

Financial managers were also asked about the development of payment delays during the previous three months, an estimate of the amount of credit losses and the companies’ willingness to invest in the next 12 months.

Based on the answers, customer payment delays have been somewhat increasing. At the same time, 30 percent of respondents predict that credit losses will increase in the coming months.

Lauri Kosloff, CFO of Zolva Finland

– For some companies, the development is worrying and certainly requires active risk management measures. On the other hand, the majority of respondents estimate that the situation will remain the same as now. It can be assumed that credit risk management is generally in good shape in Finnish companies, says Kosloff.

According to him, one interesting observation from the results of the CFO barometer is related to the willingness to invest and the wide dispersion of the answers. 40 percent of the respondents believe that investments will grow in the next 12 months. The same 40 percent disagree.

– The investment perspective for the upcoming year gives little hope for the recovery of the confidence of financial decision-makers. Uncertainty in the economy and the tightening of financial market have certainly also had a significant impact on the willingness to invest. It’s interesting to see which way the outlook turns as spring progresses, says Kosloff.

Zolva’s CFO barometer was carried out in February as an online survey. There were 33 respondents.

The next CFO-Barometer survey will be conducted in April and the results of the survey will be published in May.

Zolva in brief

Founded in 2021

Previously known as Finans2 in Nordics

Groups’ estimated revenues are 50 MEUR

650 employees

Operations in Norway, Finland, Sweden, Denmark, Italy, Spain and Portugal

Consumer loans under changing environment – The biggest change after a year

, 6:49 GMT

According to Mikko Eloranta, overindebtedness is a real problem that can lead to significant negative effects on the entire national economy.

The aim of the new legislation is to tackle consumers’ over-indebtedness. Credit institutions and the collection industry are already preparing for the upcoming changes.

The over-indebtedness of consumers is now wanted to be controlled by means of legislation. In the background, there is a negative cycle that has been going on for years, where the number of individuals who have defaulted on payments has increased.

According to Asiakastieto, more than 365,000 Finns have a payment default entry in their credit information, although the amendment to the Credit Information Act, that came into effect at the end of last year, removed almost 20,000 people from the register. The Bank of Finland’s database, on the other hand, reveals that the portfolio of unsecured consumer loans was 8.5 billion euros at the end of the year.

“Hopefully, the new guidelines for good collection practices will increase transparency and leave no room for interpretation. At Zolva we want to promote responsibility for the entire debt collection industry.”

MIKKO ELORANTA, HEAD OF LEGAL

Changes in legislation will also have an effect for secured and unsecured consumer credits and debt collection agencies. Collection company Zolva’s Head of Legal Mikko Eloranta lists the most important changes below.

Positive credit information register and interest rate cap

The usage of the positive credit information register in consumer lending will start on 1st of April 2024. The positive credit information register means that all lenders are obliged to report the credits taken by the consumer to a common register maintained by the authority. Credit register data can also be combined with income register data.

In the future, lenders will be aware of how much credit the consumer has to various financial institutions and what his or her ability to pay is in relation to the amount of credit.

– The register contains information on, among other things, on granted loans, loan principal, interest rates, payment delays for more than 60 days and information on debt recovery proceedings. This is a very positive thing. I strongly believe that a positive credit information register will decrease over-indebtedness. At the same time, it will reduce the credit losses for credit institutions, says Eloranta.

According to him, a positive credit information register should be introduced instead of lowering the interest rate ceiling. The planned amendment to the Consumer Protection Act will lower the maximum interest rate on consumer loans from the current 20 percent to 15 percent.

The law should enter into force later this year. In the government’s proposal, the transition period is six months.

– Especially in the current economic situation, it would make more sense to regulate lenders in a different way than with an interest rate cap. The danger is that when the price of money is high, granting unsecured credit becomes unprofitable. It affects consumers and the market negatively, Eloranta estimates.

Payment remarks were wiped off all at once from thousands of those who received a payment remark, when the change in the Credit Information Act came into effect at the beginning of December.

In the future, the marking will be removed one month after the consumer has paid his or her debt and the debtor has reported the information to the credit information company. The aim of the law change is to encourage consumers to pay their debts regularly and to speed up the return to a “normal” situation.

The change in the law has an impact on us and our clients. We no longer receive information about the consumer’s previous payment behavior in the same way through payment remarks. This information is valuable if the person’s payment defaults have been frequent. And many of those who have received a notice of payment default have had problems with payments for a long time, says Eloranta.

Guidelines for good practice in debt collection

The Finnish Competition and Consumer Authority’s guidance on good debt collection practices in consumer debt collection is changing. The draft is currently in the opinion round.

According to Eloranta, the current guidelines are open to interpretation. The guidelines have been valid since 2014. Since then, for example, various digital payment methods have become more commonly used.

Because of the instructions have been open to different interpretations, some debt collection companies have unintentionally acted against the instructions.

Zolva in brief

Perustettu 2021

Previously know as Finans2 in Nordics

Groups’ estimated revenues are 50 MEUR

650 employees

Operations in Norway, Finland, Sweden, Denmark, Italy, Spain and Portugal

– One open to interpretation has been related to the fact that disputed receivables cannot be collected. At what stage can the debt collection company check whether the dispute is invalid and the debt collection can be continued? It cannot be the case that the debtor simply disputes a claim without any grounds. Hopefully, the new guidelines for good practice in debt collection will increase transparency and leave no room for interpretation. It has an impact on the industry’s reputation. At Zolva we want to promote responsibility for the entire debt collection industry, says Eloranta.

The activities of debt collection companies are regulated by the Debt Collection Act. The law states that collection may not use procedures contrary to good collection practices. The guidelines published by the Finnish Competition and Consumer Authority aim to set a framework for debt collection companies’ procedures. However, market law decides on the content of good debt collection practices.

Other actions

Less attention has been paid to the Omnibus Directive initiatited through EU, which has been incorporated into Finnish legislation through changes to the Consumer Protection Act. For example, regulation of distance sales have been tightened, and transparency has been added to online store discount campaigns and product reviews.

– The aim of the legislation is to improve the position and security of consumers. For example, a contract made over the phone will only be valid in the future if the consumer has accepted the contract in writing after the call, says Eloranta.

In addition, a pilot project is underway, the goal of which is to increase the purchasing power of debtors in the weakest position. Bailiffs’ Office has started a pilot project, where the protection share of the protected income has been increased by approximately 190 euros per month.

At the same time, the number of payment-free months for low-income people in Bailiffs’ Office will permanently change to three months. On special grounds, a debtor with a low income can also be granted a fourth payment free month. The change will take effect in May.

– The measures are understandable in this economic situation. The wish is that the real benefits are also investigated and analyzed thoroughly. Otherwise, the recovery from overdue debts will only be prolonged, Eloranta estimates.

Turo Rytsölä: A new direction for the debt collection industry

03 Mar 2023, 7:27 GMT

"Debt collection industry needs a new direction".

This is what debt collection company Zolva's Head of Sales Turo Rytsölä says.

Rytsölä is one of the members of Zolva’s local management team. He is responsible for sales and marketing in Finland.

The collection industry needs a new direction.

This is what debt collection company Zolva’s Head of Sales Turo Rytsölä says.

– The interests of clients, end customers and debt collection companies must be aligned. At the moment it is not happening. We have received a strong message from our customers that the willingness to develop cooperation, especially among the large debt collectors, has been low, he says.

Rytsölä refers to, among other things, transparency. The operations and processes in the industry are not transparent towards the clients,, so the efficiency of the collection process remains unclear. Fees charged to end customers are also often obscured.

As an end-result, the reputation of the entire industry remains weak.

“Our goal is to be a major player in Finland. There is a lot of potential and opportunities. I believe that we will hire 10–20 people in Finland by the end of this year. We are looking for experts especially in receivables management and customer service.”

TURO RYTSÖLÄ, HEAD OF SALES

– The industry would have tools and opportunity to act differently. Methods of handling payments familiar from today’s banking world could also be used in the debt collection industry. Otherwise, the activities towards end customers for paying invoices must be on a completely different level. We are able to offer all the most commonly used payment methods and channels as well as flexible payment plans for paying the unpaid invoice. It improves the customer experience.

Flexibility, modern technology and real-time data transfers

Rytsölä emphasizes the opportunity for clients to make choices. Every collection process can be agreed on a customer-specific basis thanks to a flexible system and modern technology.

The utilization of data is key for success. Data and information related to assignments are transferred in real time between different systems and databases when it comes to transferring an invoice to collection, making a payment, status information or reporting.

– As a result, many things become easier and transparent, such as invoice management, payment and cash flow monitoring, he lists.

Zolva Group is a new player in Finland and internationally. However, the turnover forecast of the company founded in the second year for last year was already almost 50 million euros. Growth has mainly come through acquisitions.

In addition to the Nordic countries, Zolva has operations in Italy, Spain, Portugal and Luxembourg. The company’s headquarters are located in Norway.

– Our goal is to be a major player in Finland. There is a lot of potential and opportunities. I believe that we will hire 10–20 people in Finland by the end of this year. We are looking for experts especially in receivables management and customer service, says Rytsölä.

Rytsölä himself has almost 25 years of experience in the industry in various sales and sales management positions. According to Rytsölä, all members of the management team have a long history in the industry and the same desire to change the industry.

Zolva’s slogan sums up the desire for change well: “Because the collection industry must change”.

– All Zolva employees have been driving in the same direction from the beginning. I myself have been able to do a little bit of everything in the beginning, and the growth phase is really interesting. Personally, this has been a unique experience, he admits.

Zolva in brief

Founded in 2021

Previously known in Nordics under name of Finans2

Group’s revenues estimated to be 50 MEUR

650 employees

Operations in Norway, Finland, Sweden, Denmark, Italy, Spain and Portugal

Endre Rangnes partners with a financial giant to introduce a new competitor in the credit management industry. New owners will provide more than NOK 4,2 billion.

The new company of Endre Rangnes, Finans2, partners with one of Brazil`s wealthiest families. Together, they have recently made their first acquisition. In the long run, the family will provide more than NOK 4,2 billion.

Endre Rangnes partners with a financial giant to introduce a new competitor in the credit management industry. This spring Aleph Capital Partners made an agreement with Bank2 to acquire Finans2. The ambition is to use Finans2 as a starting point for further expansion in the European market. Finans2 will be managed by CEO Endre Rangnes, while Jon Harald Nordbrekken becomes the Chairman. Both Rangnes and Nordbrekken are also involved as investors.

Together they will create new pan-European platform with the desire to become a significant pan-European NPL purchaser and servicer.

“We will most definitely benefit from Safra Group`s financial muscles and expertise. The partnership will give us many opportunities in the future”

ENDRE RANGNES, CEO.

Enters the market with NOK 4,2 billion

After a period of negotiations Finans2 agreed upon an extensive partnership with J. Safra Group, an international conglomerate controlled by the Safra family. J. Safra Group is committed to contribute with 400 million euros, equivalent to NOK 4,2 billion. Rangnes says the company most likely will provide significantly more capital in the long run.

“The credit management industry is fragmented and barely consolidated. We want to consolidate in the long run. As such, there is a need for more capital”, says Rangnes to Finansavisen. J. Safra Group is a leading company within the industry, and the family-owned conglomerate owns banks and companies across the world. The Group has 270 billion dollars in total assets and 20 billion dollars in equity. Read more about J. Safra Group.

Pertnership will add new opportunities

“By having J. Safra Group on board we have a solid financial backing. The Group will be involved in all our purchases to ensure a good return on invested capital”, says Rangnes.

Joseph Safra, the founder of J. Safra Group died last year, 82 years old. He was the wealthiest banker in the world and the richest man in Brazil. According to Forbes, Joseph had a fortune of 13.8 billion dollars in 2020. The conglomerate currently consists of the following banks: Banco Safra, the sixth largest bank in Brazil, J. Safra Sarasin, the sixth largest bank in Switzerland and Safra National Bank of New York.

“We will most definitely benefit from Safra Group`s financial muscles and expertise. The partnership will give us many opportunities in the future”, says Rangnes.

Finans2 has offices in Norway, Sweden and Denmark. The ambition is to rapidly establish a presence in six to seven countries within a short period of time. The new group has recently made its first acquisition outside the Nordic region, the Iberian company Multigestion.

“With the acquisition of Multigestion, we are acquiring a solid platform in Spain and Portugal and will be well positioned in the financial services segment, focusing both on third party collections and portfolio acquisitions.” Multigestion is a well-established player in the Iberian NPL markets, having operated in Spain and Portugal for close to 30 years. Multigestion has scale, bringing with it circa 250 employees and EUR 5.7 billion of NPLs under management as a third-party collection provider, and mainly serves the financial services sector. Last year the company had a revenue of 8 million euros.

“Previously, Multigestion has not bought non-performing portfolios. We are now scaling up this work”, says Rangnes. Rangnes has recruited the former Spanish CEO at Axactor to be in charge of the scale up in Iberia.

Investment in nutshell

More than NOK 4,2 billion for investments

Enables geographical expansion

First acquisition made in Spain

Ambition to establish presence in six to seven countries within short period of time

New ownership structure

Safra Group`s financial muscles and expertise. The partnership will give us many opportunities in the future.

Aleph Capital and Safra Group enters the partnership with 20 million euros each. As such, they will get an 80 percent ownership share in Finans2. Nordbrekken and Rangnes enters the company with a total of 5 million euros, giving them 20 percent ownership.

Buys portfolio in Spain

Initially, Aleph Capital and Safra Gorup enters the partnership with 20 million euros each. As such, they will get an 80 percent ownership share in Finans2. Nordbrekken and Rangnes enters the company with a total of 5 million euros, giving them 20 percent ownership.

“Going forward, J. Safra Group will provide significant equity making them the largest owner”, says Rangnes. In addition to Multigestion, the new platform has also made its first acquisition of a Spanish unsecured NPL portfolio. The portfolio has an outstanding principal of EUR 3.16 billion and consists of 650 000 claims. The portfolio will be managed by Multigestion.

“With the acquistion of Multigestion, Finans2 is already present in five countries. Our initial aim is to expand in the Nordics and Iberia. In parallel, we are working with two/three other countries. We want to enter larger markets such as Italy, France and Germany”, says Rangnes.

The ambition is to create a leading pan-European non-performing loan platform and collection agency.

Aleph Capital and the J. Safra Group have entered into a strategic partnership to create a leading pan-European non-performing loan platform and debt collection agency

Aleph Capital Partners LLP (“Aleph”) and the J. Safra Group are pleased to announce that they have entered into a strategic partnership to create a leading pan-European non-performing loan platform and debt collection agency. The platform will focus on servicing and purchasing unsecured non-performing loan (“NPL”) portfolios through partnerships with financial institutions throughout Europe. The platform will be led by CEO Endre Rangnes and a new management team gathered under his leadership. Jon Harald Nordbrekken will become the Chairman of the new platform.

“With the acquisition of the Multigestion, we are acquiring a solid platform in Spain and Portugal and will be well positioned in the financial services segment, focusing both on third party collections and portfolio acquisitions”.

– Endre Rangnes, CEO.

Strategic partnership enables geographical growth

As part of this strategic partnership, Aleph and the J. Safra Group are pleased to announce the signing of definitive documentation to purchase Multigestion Iberia S.L.U. (“Multigestion”). In March 2021, a fund backed by Aleph had announced the agreement to acquire Finans2 in Norway. Multigestion and Finans2, pending receipt of regulatory approval in Norway, will be both integrated into the new pan-European platform by the management team led by CEO Endre Rangnes. The acquisition of Multigestion marks the next key milestone in the development of the platform as it establishes itself as a significant pan-European NPL purchaser and servicer.

Multigestion has solid track record in Iberian market

Multigestion is a well-established player in the Iberian NPL markets, having operated in Spain and Portugal for close to 30 years. Multigestion has scale, bringing with it circa 250 employees and EUR 5.7 billion of NPLs under management as a third-party collection provider (3PC), and mainly serves the financial services sector. Finally, Multigestion has developed a highly scalable collection platform and has invested significantly in new collection processes over the past 3 years.

In addition to Multigestion, the new platform has also made its first acquisition of a Spanish unsecured NPL portfolio. The portfolio has an outstanding principal of EUR 3.16 billion and consists of 650 000 claims. The portfolio will be managed by Multigestion.

According to the European Central Bank, the size of the European NPL market is expected to increase to ~EUR 1.4 trillion by end 2022. The platform’s new management team has proactively targeted Iberia as one of the first jurisdictions to expand into along with the Nordics. The ambition is to become the partner of choice to local financial institutions for the management of their unsecured NPL portfolios, whether through NPL sales or long-term scalable and flexible servicing agreements. Following the Multigestion acquisition, the new platform will be well positioned to do exactly this in Iberia.

“Multigestion is a great match for the new platform. Combining our knowledge and experience from the Spanish and Portuguese credit management industry with the group’s knowledge and financial resources will enable us to deliver a competitive debt collection offering and grow our operations to the next level“, says Jacques Llorens, CEO of Multigestion.

Multigestion in brief

30 years of knowledge in debt collection

Present in Spain and Portugal

250 employees

EUR 5.7 billion portfolio managed in 3PC

Recently acquired NPL-portfolio of EUR 3.16 billion consisting of 650.000 claims

Comments from Zolva CEO

“With the acquisition of the Multigestion, we are acquiring a solid platform in Spain and Portugal and will be well positioned in the financial services segment, focusing both on third party collections and portfolio acquisitions. We are excited to get more than 250 new colleagues and a very experienced management team on board. This acquisition is the first step in our Pan-European growth plan with focus on the financial services sector.”

Endre Ranges, CEO of Zolva Group

Closing of the acquisitions

Closing of the Multigestion and Spanish NPL transactions are not subject to any regulatory approval and are expected to occur by the end of July 2021. The acquisition of Finans2 remains subject to on-going regulatory approval by the Financial Supervisory Authority of Norway (Nw. Finanstilsynet). Once the approval is obtained the businesses will be combined into the new group structure.